I thought the video of Kathryn Schultz was well worth the time to watch. In a lot of ways it can be easily connected to our current toxic political environment, and the type of environment that leads to catastrophic errors in calculations by so called experts.

Saturday, May 7, 2011

Tuesday, May 3, 2011

Good Article on Commodities

I came across this little report recently that reaffirms some of my long term views about the future. The single largest problem our world faces is population growth and the demand on resources this presents. Oil production is really the major factor that has allowed world populations to grow at the rate they have grown. The developments in seeds and fertilizers are also responsible. I think we are going to find that we will soon be, (if we haven't already) experiencing limits to oil and fertilizer production that simply cannot keep up with expanding population growth. China realizes this. They invest heavily in trying to maintain their future supplies of these resources. This is going to mean long term prices are going to be going up, and in my opinion probably a large drop in standard of living for the next generation.

Read the article. It's worth your time.

Link to article

Read the article. It's worth your time.

Link to article

Sunday, May 1, 2011

GB9A Relative Strength Portfolio

Here is a relative strength portfolio that I just started trading. I'll explain what it is and the rationale for using it.

The portfolio uses 9 asset classes. DBC (Commodities), EEM (Emerging Markets), EFA (EAFE index), IAU (Gold), SH (Short S&P), SPY (S&P 500), TIP (Inflation protected treasuries), TLT (15 year treasury), VNQ (real estate).

Why so few etfs? I've found that packing too many etfs into a relative strength portfolio doesn't add performance. It actually hinders it from rotating to the best performing sector. It's best to keep it simple and not over complicate it by adding similar asset classes with slightly different shades. Some people like to create separate portfolios for bonds, international stocks, and US stocks. That is typical asset allocation. However, I would like to point out that in a bull market your bond allocation will be in high yield bonds which don't provide you the traditional protection that treasury bonds add. Your asset allocation won't protect you in the same way a fixed asset allocation will. So in this light I'd rather go with one portfolio and let it rotate to the best asset class.

How many to hold? I'm selecting the top 2 asset classes from the list. Why? The top 2 provides a little more stability to the returns while still allowing the portfolio to completely exit an asset class. Using 3 etfs in such a small portfolio means you have to hold an under performing asset class. To hold more asset classes you need a larger portfolio.

How is the relative strength calculated? It is calculated using the 3 month price performance weighting this calculation at 70 percent. It also uses the 20 say volatility weighting this calculation at 30 percent. I've back tested 6 month price performance the the draw downs are much higher. The 3 month catches the big trends but adapts fast enough to get you out of an asset class as it begins to lose favor. A smaller time frame can help you get out even sooner but you will get whipped around more and it doesn't seem to help overall returns. The volatility filter helps reduce draw downs and provides more stable returns. As the volatility of an etf increases it's rank will be pushed lower. Volatility eats into returns and is also a sign that an asset class is beginning to fail. It will hurt overall returns but will reduce risk and draw downs. I think I've found a good balance with this weighting.

How often do you update the portfolio? The portfolio is updated once per month. Updating more often doesn't increase returns, nor does it reduce risk. You only whipsaw yourself. No stops are used but I will start calculating an equity curve and see if that helps reduce draw down and risk.

What about risk management? That's up to you. You can use stops, and equity curve, puts, nothing or a combo. I'm going to let it run without stops and trust that the portfolio to rotate as it is designed into treasuries, or an S&P short if the market dives. I like using cheap out of the money puts to protect against major catastrophes in excess of 30 percent losses. Less than that I'll let the portfolio run and rotate me out into safety at the beginning of each month.

Important Notes About the Back Test

The max draw down on the performance graphs is calculated monthly. It is not your true max draw down. During the month the portfolio could draw down much greater than 15 percent. All the performance test is showing you is that from month to month it never exceeded 15 percent, but it could have drawn down 30 percent or more during the month. A couple of the etfs on the list did not exist before 2006 so the performance before 2006 would be impacted by this.

So in a nutshell here are the rules.

1) Buy the top 2 etfs in the portfolio according to the above ranking rules

2) Update the holdings once per month. If the etfs being held are no longer the top 2 performers they are sold and replaced by the new top 2 performers. If nothing has changed in the rankings then nothing is bought or sold that month.

3) Take the good and the bad. Sit tight and let the portfolio work. It will out perform at times, and also correct sooner or larger than the overall market at times.

I'm trading this portfolio and I'll keep updates on the 1st of the month on it's progress. I'll also post some more info on this portfolio and additional tests as I go along.

The portfolio uses 9 asset classes. DBC (Commodities), EEM (Emerging Markets), EFA (EAFE index), IAU (Gold), SH (Short S&P), SPY (S&P 500), TIP (Inflation protected treasuries), TLT (15 year treasury), VNQ (real estate).

Why so few etfs? I've found that packing too many etfs into a relative strength portfolio doesn't add performance. It actually hinders it from rotating to the best performing sector. It's best to keep it simple and not over complicate it by adding similar asset classes with slightly different shades. Some people like to create separate portfolios for bonds, international stocks, and US stocks. That is typical asset allocation. However, I would like to point out that in a bull market your bond allocation will be in high yield bonds which don't provide you the traditional protection that treasury bonds add. Your asset allocation won't protect you in the same way a fixed asset allocation will. So in this light I'd rather go with one portfolio and let it rotate to the best asset class.

How many to hold? I'm selecting the top 2 asset classes from the list. Why? The top 2 provides a little more stability to the returns while still allowing the portfolio to completely exit an asset class. Using 3 etfs in such a small portfolio means you have to hold an under performing asset class. To hold more asset classes you need a larger portfolio.

How is the relative strength calculated? It is calculated using the 3 month price performance weighting this calculation at 70 percent. It also uses the 20 say volatility weighting this calculation at 30 percent. I've back tested 6 month price performance the the draw downs are much higher. The 3 month catches the big trends but adapts fast enough to get you out of an asset class as it begins to lose favor. A smaller time frame can help you get out even sooner but you will get whipped around more and it doesn't seem to help overall returns. The volatility filter helps reduce draw downs and provides more stable returns. As the volatility of an etf increases it's rank will be pushed lower. Volatility eats into returns and is also a sign that an asset class is beginning to fail. It will hurt overall returns but will reduce risk and draw downs. I think I've found a good balance with this weighting.

How often do you update the portfolio? The portfolio is updated once per month. Updating more often doesn't increase returns, nor does it reduce risk. You only whipsaw yourself. No stops are used but I will start calculating an equity curve and see if that helps reduce draw down and risk.

What about risk management? That's up to you. You can use stops, and equity curve, puts, nothing or a combo. I'm going to let it run without stops and trust that the portfolio to rotate as it is designed into treasuries, or an S&P short if the market dives. I like using cheap out of the money puts to protect against major catastrophes in excess of 30 percent losses. Less than that I'll let the portfolio run and rotate me out into safety at the beginning of each month.

Important Notes About the Back Test

The max draw down on the performance graphs is calculated monthly. It is not your true max draw down. During the month the portfolio could draw down much greater than 15 percent. All the performance test is showing you is that from month to month it never exceeded 15 percent, but it could have drawn down 30 percent or more during the month. A couple of the etfs on the list did not exist before 2006 so the performance before 2006 would be impacted by this.

So in a nutshell here are the rules.

1) Buy the top 2 etfs in the portfolio according to the above ranking rules

2) Update the holdings once per month. If the etfs being held are no longer the top 2 performers they are sold and replaced by the new top 2 performers. If nothing has changed in the rankings then nothing is bought or sold that month.

3) Take the good and the bad. Sit tight and let the portfolio work. It will out perform at times, and also correct sooner or larger than the overall market at times.

I'm trading this portfolio and I'll keep updates on the 1st of the month on it's progress. I'll also post some more info on this portfolio and additional tests as I go along.

Thursday, April 28, 2011

This Credit Rating Agency Has it Right

I've wondered for quite some time how the United States with a 12+ trillion dollar debt, has maintained a credit rating higher than China, a country with a huge mega surplus of cash. It makes no sense. We all know about the S&P threats to lower the US credit rating but one credit agency has gone ahead and rated it the way it should be. China should be ranked higher than the US in credit. The US takes it's rightful place with countries like Brazil and Japan. By the time we wake up and realize we have a problem it will be far too late. I'm glad my portfolio is very protected against inflation.

http://www.marketwatch.com/story/us-gets-c-credit-rating-lower-than-mexico-2011-04-28

http://www.marketwatch.com/story/us-gets-c-credit-rating-lower-than-mexico-2011-04-28

Thursday, April 21, 2011

The Ivy Portfolio Review and Tests

The Ivy Portfolio by Mebane Faber is a great read and is a staple reference in my library.

Take a look at this chart:

I'd say that's a pretty decent return on a strategy since 2008. + 36% return vs. -3.6% on the S&P 500. The above is a simple back test of a strategy from the Ivy Portfolio that I did on etfreplay. It uses the 19 asset Ivy Portfolio which performed better on the moving average model than the portfolios with less asset classes. I want to point out that this portfolio goes back only to 2008 where market timing clearly had a big advantage. Longer term numbers are decent but not like the above. You can expect to beat buy and hold with less draw down by about a percent per year but not destroy it like the above test may lead you to believe. Probably charts like the above have sparked interest in using moving averages to reduce risk in portfolios. Do they work on lengthier horizons? According to the Ivy Portfolio book the answer is yes. According to my own back testing results the answer is also yes.

I'd say that's a pretty decent return on a strategy since 2008. + 36% return vs. -3.6% on the S&P 500. The above is a simple back test of a strategy from the Ivy Portfolio that I did on etfreplay. It uses the 19 asset Ivy Portfolio which performed better on the moving average model than the portfolios with less asset classes. I want to point out that this portfolio goes back only to 2008 where market timing clearly had a big advantage. Longer term numbers are decent but not like the above. You can expect to beat buy and hold with less draw down by about a percent per year but not destroy it like the above test may lead you to believe. Probably charts like the above have sparked interest in using moving averages to reduce risk in portfolios. Do they work on lengthier horizons? According to the Ivy Portfolio book the answer is yes. According to my own back testing results the answer is also yes.

There are two main investing ideas in the book - Diversity through asset allocation, and simple market timing to avoid bear markets. Faber goes into detail on how the endowments invest in various asset classes which helps bring more stable returns with less draw downs. (2008 was a bad year for the endowments because essentially all asset classes failed except treasuries. Asset allocation still helped but was much less effective)

The simplest allocation is us stocks, international stocks, real estate, and commodities. (Invest in etfs obviously not rip off mutual funds) The more complex portfolios essentially sub-divide those asset classes into finer cross sections. The discussion on these ideas is very good but of even more interest to me is the timing model Faber promotes in the book.

The timing model is incredibly simple but performs well. When the asset class is above the 280 day moving average you buy that asset class. If it is below the 280 day moving average you sell that asset class and move into cash. Just the percentage of the portfolio dedicated to that asset class would be in cash. Larry Connors uses the 200 day moving average in virtually all of his swing trading strategies. He's found having the long term trend at your back helps reduce risk. I do want to point out though, that Connors is not a fan of moving cross over strategies. He questions the longer term results Link

Robert Colby's work in his book the Encyclopedia of Technical Market Indicators shows his back testing results on simple moving average systems like this with very positive results going very far back in time vs buy and hold.

Using these moving average systems seems to reduce risk but can be prone to whipsaw in sideways market. There appears to be a fairly simple solution to this problem.

In Faber's models he updates the portfolio once per month. Buys and sells are only done once per month regardless of any signals during the month. At first I thought this was just to make it easy to manage. After testing specifically if it made a difference I found it actually improved performance significantly. The reason is simple. You don't get whipsawed buying then selling the position around the moving average as it moves back and forth. I was surprised that simply buying on the same day each month improved performance so much. There might be even better ways to avoid whipsaw like waiting x amount of days after a cross over to make a position change to make sure the trend change is real but I have not tinkered with that. The monthly management method works well and is far easier to work with.

Here are some of my own testing results below:

The first chart takes all signals on any day of the month on the $spx index. If the price closes below the 280 day moving average it is sold, and if it crosses above the 280 day moving average the market is bought.

You can't buy shares of the pure index so the dollar amounts are more about comparing the two results than actual returns.

You can see some evidence of whipsaw eating into profits on the chart. The back test goes too far back to get it all in on this chart though.

You can see some evidence of whipsaw eating into profits on the chart. The back test goes too far back to get it all in on this chart though.

Here is the once a months management method. Performance is much better.

Here is the once a months management method. Performance is much better.

Less whipsaw and fake outs.

If you don't have the book, here is link to Faber's paper on market timing relative strength model. link

Take a look at this chart:

There are two main investing ideas in the book - Diversity through asset allocation, and simple market timing to avoid bear markets. Faber goes into detail on how the endowments invest in various asset classes which helps bring more stable returns with less draw downs. (2008 was a bad year for the endowments because essentially all asset classes failed except treasuries. Asset allocation still helped but was much less effective)

The simplest allocation is us stocks, international stocks, real estate, and commodities. (Invest in etfs obviously not rip off mutual funds) The more complex portfolios essentially sub-divide those asset classes into finer cross sections. The discussion on these ideas is very good but of even more interest to me is the timing model Faber promotes in the book.

The timing model is incredibly simple but performs well. When the asset class is above the 280 day moving average you buy that asset class. If it is below the 280 day moving average you sell that asset class and move into cash. Just the percentage of the portfolio dedicated to that asset class would be in cash. Larry Connors uses the 200 day moving average in virtually all of his swing trading strategies. He's found having the long term trend at your back helps reduce risk. I do want to point out though, that Connors is not a fan of moving cross over strategies. He questions the longer term results Link

Robert Colby's work in his book the Encyclopedia of Technical Market Indicators shows his back testing results on simple moving average systems like this with very positive results going very far back in time vs buy and hold.

Using these moving average systems seems to reduce risk but can be prone to whipsaw in sideways market. There appears to be a fairly simple solution to this problem.

In Faber's models he updates the portfolio once per month. Buys and sells are only done once per month regardless of any signals during the month. At first I thought this was just to make it easy to manage. After testing specifically if it made a difference I found it actually improved performance significantly. The reason is simple. You don't get whipsawed buying then selling the position around the moving average as it moves back and forth. I was surprised that simply buying on the same day each month improved performance so much. There might be even better ways to avoid whipsaw like waiting x amount of days after a cross over to make a position change to make sure the trend change is real but I have not tinkered with that. The monthly management method works well and is far easier to work with.

Here are some of my own testing results below:

The first chart takes all signals on any day of the month on the $spx index. If the price closes below the 280 day moving average it is sold, and if it crosses above the 280 day moving average the market is bought.

You can't buy shares of the pure index so the dollar amounts are more about comparing the two results than actual returns.

Less whipsaw and fake outs.

Overall I think this is a good system to be using. I'm using it in conjunction with the relative strength models I often post about. You can actually combine the two models but I run them as separate portfolios.

I want to point out that I've done tests using a 120 day exponential moving average and got good results. It might be worth looking at that time frame as well.

Sunday, April 17, 2011

Inflation

If you look at the government numbers we have minimal inflation. Remember back when gas was hitting $4.50 - $5.00 a gallon in some places and food and health care costs were also going up just as fast? The government reported next to no inflation. It was a joke.

The government has been slowly devaluing your currency for ages and they changed the way they report inflation to keep you in the dark. I came across this article today which looks at the way the government used to report inflation, and if they still did it this way today inflation would be over 10 percent, which seems in line with what I'm seeing in my day to day expenses. article

Peter Schiff talks about how the government reports inflation quite a lot in his book Crash Proof. I've been a big fan of Peter Schiff, though I find it sad someone who saw the stock market crash coming couldn't make a profit from it, but I digress...

Another piece of evidence for inflation if through the permanent portfolio. The permanent portfolio divides assets into 5 categories and equal weights them. Precious metals, commodities, growth stocks, treasuries, and swiss franc assets. The ticker is prpfx. It's a mutual fund based on the Harry Browne concept of the permanent portfolio.

The government has been slowly devaluing your currency for ages and they changed the way they report inflation to keep you in the dark. I came across this article today which looks at the way the government used to report inflation, and if they still did it this way today inflation would be over 10 percent, which seems in line with what I'm seeing in my day to day expenses. article

Peter Schiff talks about how the government reports inflation quite a lot in his book Crash Proof. I've been a big fan of Peter Schiff, though I find it sad someone who saw the stock market crash coming couldn't make a profit from it, but I digress...

Another piece of evidence for inflation if through the permanent portfolio. The permanent portfolio divides assets into 5 categories and equal weights them. Precious metals, commodities, growth stocks, treasuries, and swiss franc assets. The ticker is prpfx. It's a mutual fund based on the Harry Browne concept of the permanent portfolio.

This fund is designed to beat inflation by a couple of percentage points. Why has it been on fire the past decade? It's because inflation has been a lot higher than people want to believe in my opinion. It's done it's job staying ahead of inflation by a couple of percentage points. Sure the chart looks like the fund is kicking @#$ and taking number but not so much when real inflation is taken into account. It probably demonstrates that people are afraid of the prospect of their long term savings losing value.

We are becoming poorer every year without realizing it. The sad thing is that when the government is forced to stop printing money things are going to get ugly because we will face the implosion of our service economy. It's a no win situation.

Relative Strength Investing Weekly Update April 17th

In the Smarter Investing Relative Strength Portfolio I'm running, I had 2 stop outs. One was in IYE, and the other was in IWR.

New buys to be placed for Monday are:

Asset Allocation Portfolio - IAU - I cringe a little at this one but the rules say buy so I buy.

Sector Allocation Portfolio - IYE - Just got stopped out but it's the number one rank. The whipsaw is a little costly since I missed the rally in it on Friday.

I am torn about using stops with this portfolio for a number of reasons. Whipsaw is the primary one. I decided I would try to follow the plan that Michael Carr put forth in his book Smarter Investing in Any Economy which uses stops. I will keep to this plan and see how it works moving forward. The portfolio should beat the market regardless and will have a much lower draw down than other relative strength investors are probably used to.

I have , however, been doing some more research and put together a method which would not be using stops has a less frequent updating time and is easier to implement. The testing results look good and I'm about ready to go forward with it soon. I plan to put out a post with my test results. I'll also at some point put together some more systematic way to track results. The nice thing is that I can run an unlimited number of portfolios in foliofn and run them independently all free of commission during their trade windows.

The method for calculating relative strength used in this portfolio is the ratio of multiple moving averages. Carr's back testing goes further back than historical etfs since he used mutual fund data and I'm confident in his testing methods. I wish I could duplicate them, but my trading / back testing software cannot make relative strength comparisons between different markets. Check older posts for more details on this method.

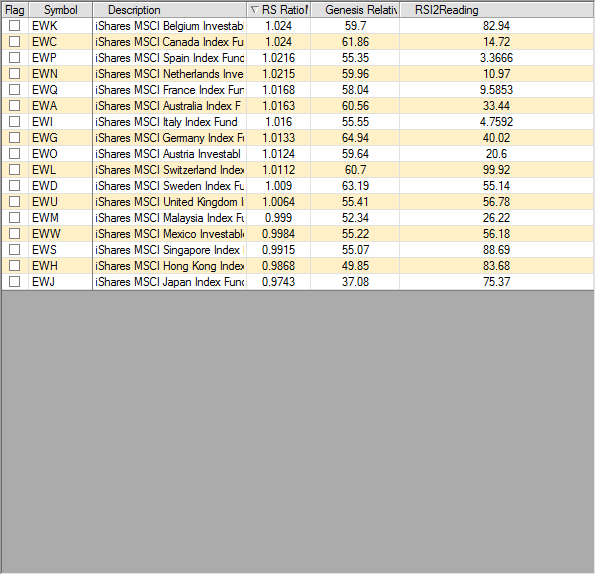

The column for the relative strength multiple moving average is the center one that starts with RS.

New buys to be placed for Monday are:

Asset Allocation Portfolio - IAU - I cringe a little at this one but the rules say buy so I buy.

Sector Allocation Portfolio - IYE - Just got stopped out but it's the number one rank. The whipsaw is a little costly since I missed the rally in it on Friday.

I am torn about using stops with this portfolio for a number of reasons. Whipsaw is the primary one. I decided I would try to follow the plan that Michael Carr put forth in his book Smarter Investing in Any Economy which uses stops. I will keep to this plan and see how it works moving forward. The portfolio should beat the market regardless and will have a much lower draw down than other relative strength investors are probably used to.

I have , however, been doing some more research and put together a method which would not be using stops has a less frequent updating time and is easier to implement. The testing results look good and I'm about ready to go forward with it soon. I plan to put out a post with my test results. I'll also at some point put together some more systematic way to track results. The nice thing is that I can run an unlimited number of portfolios in foliofn and run them independently all free of commission during their trade windows.

The method for calculating relative strength used in this portfolio is the ratio of multiple moving averages. Carr's back testing goes further back than historical etfs since he used mutual fund data and I'm confident in his testing methods. I wish I could duplicate them, but my trading / back testing software cannot make relative strength comparisons between different markets. Check older posts for more details on this method.

The column for the relative strength multiple moving average is the center one that starts with RS.

Subscribe to:

Comments (Atom)