New buys to be placed for Monday are:

Asset Allocation Portfolio - IAU - I cringe a little at this one but the rules say buy so I buy.

Sector Allocation Portfolio - IYE - Just got stopped out but it's the number one rank. The whipsaw is a little costly since I missed the rally in it on Friday.

I am torn about using stops with this portfolio for a number of reasons. Whipsaw is the primary one. I decided I would try to follow the plan that Michael Carr put forth in his book Smarter Investing in Any Economy which uses stops. I will keep to this plan and see how it works moving forward. The portfolio should beat the market regardless and will have a much lower draw down than other relative strength investors are probably used to.

I have , however, been doing some more research and put together a method which would not be using stops has a less frequent updating time and is easier to implement. The testing results look good and I'm about ready to go forward with it soon. I plan to put out a post with my test results. I'll also at some point put together some more systematic way to track results. The nice thing is that I can run an unlimited number of portfolios in foliofn and run them independently all free of commission during their trade windows.

The method for calculating relative strength used in this portfolio is the ratio of multiple moving averages. Carr's back testing goes further back than historical etfs since he used mutual fund data and I'm confident in his testing methods. I wish I could duplicate them, but my trading / back testing software cannot make relative strength comparisons between different markets. Check older posts for more details on this method.

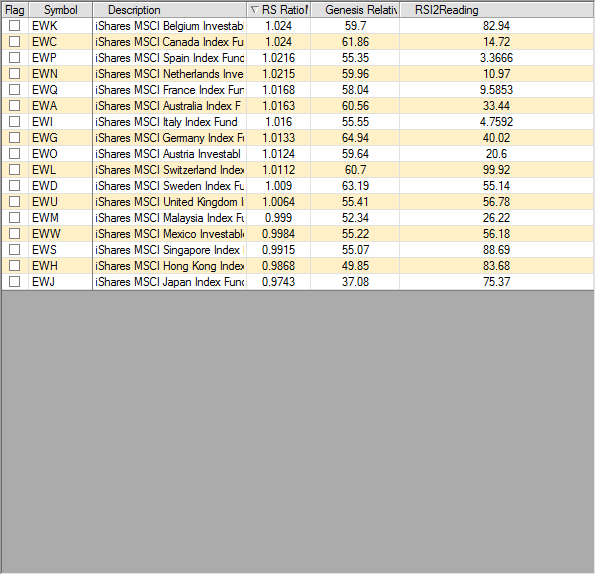

The column for the relative strength multiple moving average is the center one that starts with RS.

No comments:

Post a Comment